Whether you made $500 or $50,000 this year, if you earned freelance income, you might owe taxes—but you also might be able to reduce your bill legally with IRS-approved deductions.

Here are the top 10 write-offs every freelancer should know, based on 2025 tax rules—plus a free printable checklist at the bottom of this post.

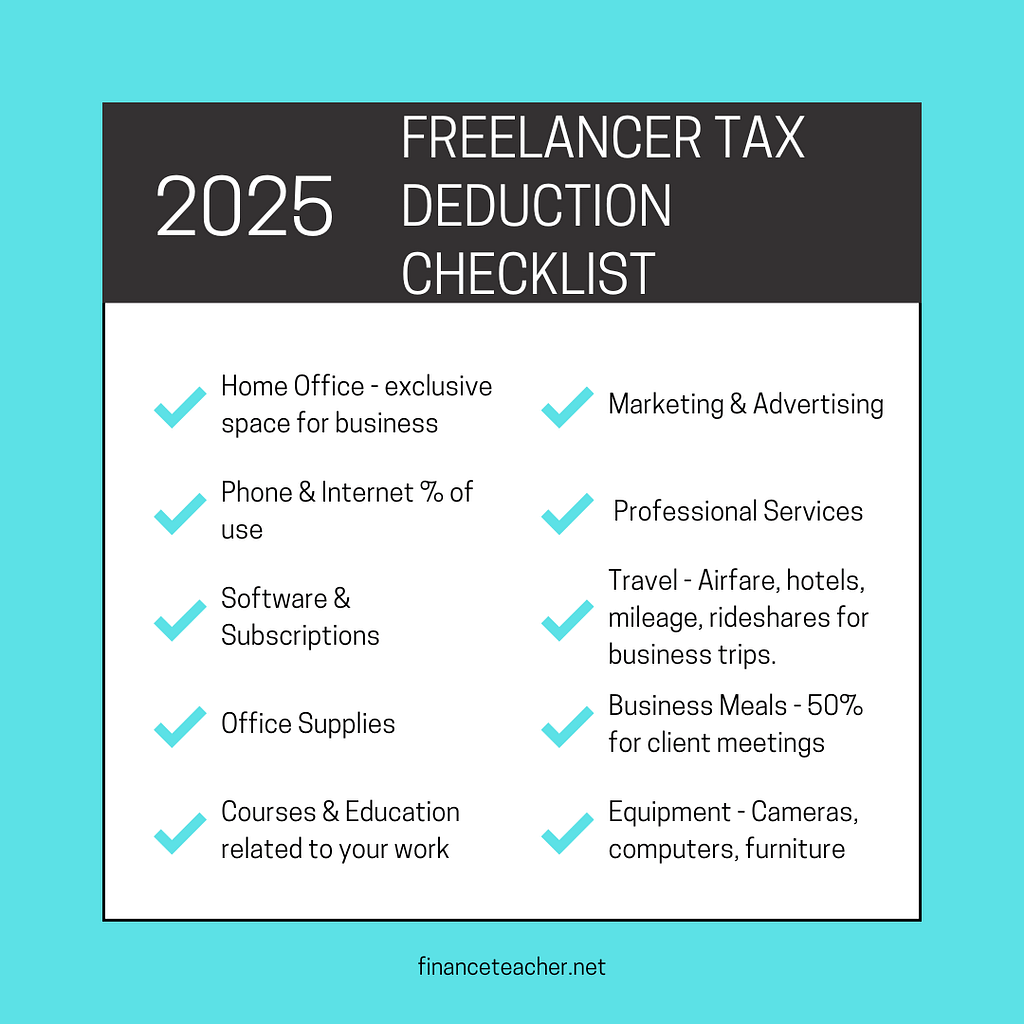

1. 🏠 Home Office Deduction

If you use a space in your home exclusively and regularly for work, you may be eligible to deduct a portion of your rent, mortgage interest, utilities, and more.

🔍 Example: If your workspace takes up 10% of your home, you can deduct 10% of qualified expenses like electricity, water, and internet.

✅ Must be a dedicated workspace. The kitchen table doesn’t count if you also eat dinner there.

2. 📱 Phone & Internet

Your cell phone and WiFi are likely used for both work and personal life. Estimate the business-use percentage (e.g., 60%), and you can deduct that portion.

📓 Pro Tip: Keep a simple log of business-related calls, texts, uploads, and meetings—no need to overcomplicate it.

3. 🧾 Software & Subscriptions

Do you pay for tools like Canva, Adobe Creative Cloud, Notion, or Zoom? If they support your business, they’re deductible.

4. 🖊️ Office Supplies

Don’t forget the little things—pens, notebooks, external hard drives, printer ink. Over time, these expenses add up.

📌 Keep your receipts and, ideally, use a business card or bank account to separate them from personal spending.

5. 🎓 Courses & Education

You can deduct classes, books, or coaching only if they relate directly to your current business. Want to become a better copywriter? That counts. Taking a real estate licensing course? Probably not.

“I had a friend who tried to write off a pottery class as a business expense because she planned to start an Etsy shop. The IRS didn’t buy it. Start the business first—then deduct qualifying education.”

6. 📣 Marketing & Advertising

Boosted a Reel? Paid for a website or logo design? Ran an Instagram or Google ad? These are all deductible as marketing expenses.

7. 👩⚖️ Professional Services

CPA, lawyer, or even bookkeeping software like QuickBooks? All tax-deductible if you use them for your freelance work.

8. ✈️ Business Travel

Traveling for a shoot, client meeting, or conference? You can usually deduct:

- Flights

- Hotels

- Rental cars

- 50% of meals

🚗 If you drive for work, keep a mileage log! Note the:

- Date

- Miles

- Purpose

- Starting/ending odometer readings for the year

In 2024, the IRS mileage rate was 67 cents per mile—2025 may differ.

9. 🍽️ Business Meals (50%)

Only meals with a client, team member, or during travel qualify. You can’t deduct lunch while working solo at home.

📲 Write the name, purpose, and date in a note or on the receipt.

10. 💻 Equipment & Depreciation

Laptops, cameras, mics, office chairs—they may be deductible.

- Under $2,500? You might be able to deduct the full amount in one year.

- Over $2,500? You may need to depreciate it over several years.

Only deduct the business-use percentage.

💄 Bonus Section: Can You Deduct Hair, Makeup & Nails?

Here’s what musicians, performers, and influencers often ask me.

| Expense | Deductible? | Why? |

|---|---|---|

| Haircuts | ❌ | Considered personal grooming |

| Eyelash Extensions | ❌ | Personal appearance |

| Nails | ❌ | Only if theatrical or prosthetic |

| Self-Tanning | ❌ | Personal grooming |

| Regular Makeup | ❌ | Everyday use |

| Theatrical Makeup | ✅ | Clearly for stage or production use |

| Costumes/Stagewear | ✅ | Not suitable for street wear |

| Photoshoots, Stylists | ✅ | Business-related branding |